Earning £100,000 a year is a milestone that puts you firmly in the top 3–4% of UK earners. It’s a figure that attracts both admiration and curiosity — and understandably so. Many people searching for “100k after tax UK” want a straightforward answer: how much of that six-figure salary actually lands in their bank account each month?

The reality is that a £100,000 gross salary is subject to several layers of deduction before it becomes your net pay. You’ll pay Income Tax across multiple bands, Class 1 National Insurance contributions, and — if applicable — student loan repayments and pension contributions. Taken together, these can reduce your take-home pay significantly.

There’s also a lesser-known issue that catches many people off-guard: the £100,000 tax trap. At exactly this income level, HMRC begins withdrawing your Personal Allowance — the amount you can earn tax-free — at a rate of £1 for every £2 you earn above £100,000. This creates an effective marginal tax rate of around 60% for income between £100,001 and £125,140, making the £100k mark one of the most tax-inefficient salary points in the UK system.

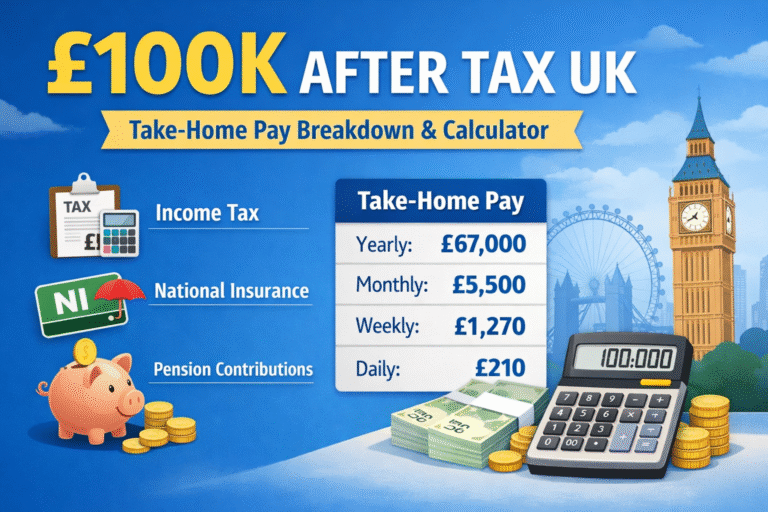

Quick summary: On a £100,000 salary, you can expect to take home approximately £66,500 – £67,562 per year after Income Tax and National Insurance, depending on your tax code and individual circumstances.

£100K After Tax in the UK — Quick Answer

If you need a fast answer, here it is. Based on the 2024/25 tax year, using the standard 1257L tax code, no pension contributions, and no student loan:

| Salary | After Tax (Yearly) | Monthly | Weekly |

| £100,000 | £66,500 – £67,000 | ~£5,500 | ~£1,270 |

These figures are estimates based on standard tax codes. Your actual take-home pay may vary depending on pension deductions, student loan repayments, bonus payments, and any other benefits or allowances relevant to your situation.

Income Tax Rates in the UK

The UK operates a progressive income tax system, meaning the more you earn, the higher the rate applied — but only to the portion of income that falls within each band. For the 2024/25 tax year, the bands are as follows:

| Tax Band | Income Range | Tax Rate | Tax Payable on £100k |

| Personal Allowance | £0 – £12,570 | 0% | £0 |

| Basic Rate | £12,571 – £50,270 | 20% | ~£7,540 |

| Higher Rate | £50,271 – £100,000 | 40% | ~£19,892 |

| Additional Rate | Over £125,140 | 45% | N/A at £100k |

On a £100,000 salary, you pass through both the Basic Rate and Higher Rate bands. Here’s a simplified calculation:

- Personal Allowance (£0 – £12,570): £0 tax

- Basic Rate band (£12,571 – £50,270): 20% on £37,700 = £7,540

- Higher Rate band (£50,271 – £100,000): 40% on £49,730 = £19,892

- Total Income Tax owed: approximately £27,432

Important: At exactly £100,000, your Personal Allowance is still fully intact. However, even £1 above this threshold begins to erode it. See Section 4 for the full explanation of the £100k tax trap.

Personal Allowance Reduction After £100K

The Personal Allowance — currently £12,570 — is the amount of income every UK taxpayer can earn completely free of Income Tax. However, for higher earners, HMRC operates what’s commonly referred to as the “£100k tax trap”.

How it works

For every £2 you earn above £100,000, your Personal Allowance is reduced by £1. This continues until the allowance is fully withdrawn at a gross income of £125,140. The table below illustrates how this affects different salary levels:

| Gross Salary | Remaining Allowance | Effective Rate Impact |

| £100,000 | £12,570 (full) | Normal |

| £106,000 | £9,570 | Rising |

| £112,570 | £6,285 | ~60% marginal rate |

| £125,140+ | £0 (none) | Fully removed |

The 60% Effective Marginal Rate

Between £100,001 and £125,140, you face a punishing marginal tax rate that most people don’t realise exists. Here’s why:

- You pay 40% Higher Rate tax on the extra pound earned.

- But you also lose £0.50 of your Personal Allowance for every £1 earned.

- That lost allowance is then taxed at 40%, adding another 20% to your effective rate.

- Combined: 40% + 20% = 60% effective marginal rate on income in this band.

This is why many high earners — and their accountants — actively work to keep their taxable income below £100,000, often through pension contributions or salary sacrifice schemes.

National Insurance on a £100K Salary

In addition to Income Tax, employees earning £100,000 must pay Class 1 National Insurance Contributions (NICs). NICs fund state benefits including the NHS, State Pension, and unemployment support. The 2024/25 rates are:

| NI Threshold | Rate | Amount Paid on £100k |

| £0 – £12,570 (LEL) | 0% | £0 |

| £12,571 – £50,270 | 8% | ~£3,014 |

| £50,271 – £100,000 | 2% | ~£992 |

| Total NI (approx) | — | ~£5,006 |

On a £100,000 salary, your total National Insurance liability is approximately £5,006. Unlike Income Tax, NICs do not carry a “personal allowance trap” — the rates simply apply to the relevant income bands.

Note that your employer also pays Employer NICs on top of your salary, currently at 13.8% above the Secondary Threshold (£9,100). This is a cost to the business, not a deduction from your pay, but it’s worth understanding the full cost of employment.

Detailed Salary Breakdown for £100K

Bringing together Income Tax and National Insurance, here is the full picture of what happens to a £100,000 gross salary under standard conditions in 2024/25:

| Category | Amount |

| Gross Salary | £100,000 |

| Income Tax | ~£27,432 |

| National Insurance (Class 1) | ~£5,006 |

| Net Take-Home (Annual) | ~£67,562 |

| Monthly Take-Home | ~£5,630 |

| Weekly Take-Home | ~£1,299 |

| Daily Take-Home (5-day week) | ~£260 |

All figures are approximations based on the standard 1257L tax code, no pension deductions, and no student loan. Monthly and weekly figures are derived by dividing the annual net figure by 12 and 52 respectively.

100k After Tax Calculator

2024/25 Tax Year · Income Tax · National Insurance · Pension · Student Loan

Your Details

Your Results

Where Your Money Goes

Estimates use 2024/25 HMRC thresholds. Pension contributions reduce taxable income (relief at source). This tool does not constitute financial or tax advice.

Because individual circumstances vary so widely, the most accurate way to determine your specific take-home pay is to use an online salary calculator. There are several excellent free tools available, including those offered by Which?, MoneySavingExpert, Listentotaxman, and the Reed salary calculator.

What information you'll need

- Gross annual salary (e.g. £100,000)

- Tax code (usually 1257L unless HMRC has issued a different one)

- Pension contribution percentage (employee and employer)

- Student loan plan type (Plan 1, 2, 4, or Postgraduate)

- Whether you receive any taxable benefits in kind

- Bonus amounts, if applicable

What the calculator will show you

- Annual net income (take-home pay)

- Total Income Tax paid

- Total National Insurance contributions

- Monthly take-home pay

- Effective (average) tax rate

- Marginal tax rate

Tip: If you're negotiating a salary increase beyond £100,000, use the calculator to model different pension contribution levels. Increasing contributions can reduce your taxable income and dramatically improve your real take-home figure.

Monthly Budget Example on a £100K Salary

With a take-home pay of approximately £5,630 per month, how far does £100,000 actually go? The answer depends heavily on where you live and your lifestyle choices. Below is a realistic monthly budget breakdown:

| Category | Monthly Cost | Notes |

| Housing (rent/mortgage) | £1,500 – £3,000 | Varies hugely by location |

| Transport | £200 – £600 | Car or season ticket |

| Utilities & Bills | £200 – £400 | Gas, electric, broadband |

| Food & Groceries | £300 – £600 | Household-dependent |

| Childcare / Education | £0 – £1,500 | If applicable |

| Leisure & Dining Out | £300 – £700 | Personal lifestyle choice |

| Pension & Savings | £500 – £1,500 | Strongly recommended |

| Remainder / Discretionary | £500 – £1,500+ | Investments, holidays, etc. |

In London, housing alone can absorb £2,000 – £3,000 or more of your monthly income, while in cities such as Leeds, Manchester, or Edinburgh, you could find comfortable accommodation for £800 – £1,400. This is the single biggest variable in your quality of life on a £100k salary.

After covering essentials in a high-cost city, a £100k earner might have £800 – £1,500 of discretionary income remaining each month. In a lower-cost region, that figure could rise to £2,000 or more, enabling faster wealth accumulation.

£100K Salary With Pension Contributions

Pension contributions are one of the most powerful tools available to £100k earners — both for retirement planning and for reducing your current tax bill. Contributions made to a workplace pension (or self-invested personal pension, SIPP) reduce your taxable income before tax is calculated.

Impact of pension contributions on take-home pay

| Contribution | Pension Deduction | Taxable Income | Est. Take-Home |

| 0% | £0 | £100,000 | ~£67,562 |

| 5% | £5,000 | £95,000 | ~£64,562 |

| 10% | £10,000 | £90,000 | ~£61,562 |

| 15% | £15,000 | £85,000 | ~£58,562 |

Key benefits of pension contributions at £100k

- They reduce your taxable income, potentially keeping you below the £100,000 threshold where the Personal Allowance withdrawal begins.

- Contributions attract 40% Higher Rate tax relief, meaning a £10,000 pension contribution effectively costs you only £6,000 net.

- If you reduce taxable income to below £100,000, you recover your full Personal Allowance, delivering an effective 60% return on that portion of contributions.

- Long-term: contributions compound tax-free within the pension wrapper until retirement.

Example: If you contribute £10,000 to your pension, your taxable income drops to £90,000. You stay well below the £100k threshold, preserve your full Personal Allowance, and save approximately £6,000 in additional tax compared to taking the full salary as cash.

£100K Salary With Student Loan Repayments

If you have a student loan, repayments are taken automatically via PAYE before you receive your pay. The amount deducted depends on which plan you're on. At a salary of £100,000, all plans will be active as you are comfortably above all repayment thresholds.

| Plan | Repayment Threshold | Rate | Est. Annual Repayment |

| Plan 1 | £24,990/yr | 9% | ~£6,751 |

| Plan 2 | £27,295/yr | 9% | ~£6,517 |

| Plan 4 | £31,395/yr | 9% | ~£6,149 |

| Postgrad | £21,000/yr | 6% | ~£4,740 |

It's important to note that student loan repayments are not tax-deductible — they come out of your post-tax income and are calculated as a percentage of earnings above the relevant threshold, not on your total salary. If you hold both an undergraduate and a Postgraduate Loan, repayments for both are collected simultaneously.

On a £100,000 salary, a Plan 2 borrower would repay approximately £6,517 per year in student loan repayments, in addition to their Income Tax and National Insurance, reducing monthly take-home to approximately £5,044.

£100K Salary vs £80K, £120K, and £150K

To understand the relative value of a £100,000 salary, it helps to compare it against similar earnings. Note how Income Tax increases disproportionately as income rises, particularly above £100,000 where the Personal Allowance withdrawal amplifies the tax burden:

| Gross Salary | Income Tax | National Insurance | Take-Home (est.) |

| £60,000 | ~£11,432 | ~£4,006 | ~£44,562 |

| £80,000 | ~£19,432 | ~£4,606 | ~£55,962 |

| £100,000 | ~£27,432 | ~£5,006 | ~£67,562 |

| £120,000 | ~£43,432 | ~£5,406 | ~£71,162 |

| £150,000 | ~£57,932 | ~£6,006 | ~£86,062 |

Notice that the jump in take-home pay from £100,000 to £120,000 is far smaller than the headline difference suggests. The £20,000 gross increase produces only around £3,600 extra in take-home pay — because the income falls in the Personal Allowance withdrawal zone where the effective marginal rate reaches 60%.

The disparity is a key reason why many employers and employees prefer to structure compensation packages using benefits, pension contributions, and bonuses rather than simple salary increases past the £100k mark.

Is £100K a Good Salary in the UK?

In absolute terms, yes — £100,000 is an excellent salary. It places you in the top 3–4% of UK earners and far exceeds the UK median salary of approximately £35,000. However, the subjective experience of "being on £100k" varies dramatically depending on individual circumstances.

London vs the Rest of the UK

In London, £100,000 is a very comfortable salary, but it does not confer the same lifestyle as it would elsewhere. A two-bedroom flat in Zone 2 or 3 can cost £2,200 – £2,800 per month to rent, childcare can be £1,500 – £2,000 per month, and general costs of living are 20–40% higher than the UK average. After these essentials, discretionary income can feel surprisingly limited.

In cities like Leeds, Birmingham, Cardiff, or Edinburgh, the same take-home pay affords a significantly more comfortable lifestyle: lower housing costs, lower transport expenses, and greater disposable income for savings and investment.

Savings potential

A disciplined £100k earner with no dependants in a moderate-cost city could realistically save £1,500 – £2,500 per month. Over ten years, with investment returns, this represents a significant wealth-building opportunity. In London with a family, realistic savings might be £500 – £1,000 per month without strict budgeting.

The perception gap

Many people earning £100,000 report that their lifestyle feels less luxurious than they expected, particularly in the early years. This is partly due to the heavy tax burden and partly due to lifestyle inflation — the natural tendency to increase spending as income rises.

Ways to Increase Take-Home Pay on £100K

There are several legitimate and HMRC-approved strategies to reduce your tax liability and improve your overall financial position on a £100,000 salary.

1. Pension Contributions (Most Effective)

As discussed in Section 9, pension contributions reduce your taxable income pound-for-pound. If you contribute enough to bring your income below £100,000, you reclaim your Personal Allowance and avoid the 60% effective marginal rate. Higher Rate taxpayers receive 40% tax relief on contributions.

2. Salary Sacrifice

Many employers offer salary sacrifice arrangements where you exchange part of your gross salary for non-cash benefits. These are paid from pre-tax income and also reduce your NI contributions. Common salary sacrifice options include additional pension contributions, cycle-to-work schemes, electric vehicle leasing, and childcare vouchers (for eligible pre-2017 schemes).

3. Gift Aid Donations

When you donate to charity through Gift Aid and declare it on your Self Assessment return, you can claim the Higher Rate relief. For every £80 you donate, the charity receives £100. As a Higher Rate taxpayer, you then reclaim an additional £20 via Self Assessment, effectively making your donation 20% cheaper.

4. ISA Contributions

Although ISA contributions don't reduce your income tax bill, they shelter future investment returns and interest from tax entirely. The annual ISA allowance is £20,000 per person. Stocks and Shares ISAs can generate tax-free returns that, over decades, can significantly outperform equivalent taxable investments.

5. Venture Capital Trusts (VCTs) and EIS

For experienced investors, Venture Capital Trusts and the Enterprise Investment Scheme offer 30% upfront income tax relief on qualifying investments (up to certain limits). These are higher-risk investments and should be approached with caution and professional advice.

6. Review Your Tax Code

It's worth checking your PAYE tax code each year to ensure it's correct. An incorrect tax code can result in overpaying tax unnecessarily. You can check and update your tax code via your Personal Tax Account on HMRC's website.

Frequently Asked Questions

What is £100k after tax per month in the UK?

Based on the 2024/25 tax year with a standard 1257L tax code, no pension contributions, and no student loan, a £100,000 salary produces a monthly take-home pay of approximately £5,630. This figure will be lower if you have student loan repayments or make pension contributions from your salary.

How much tax do you pay on £100k in the UK?

On a £100,000 salary, you pay approximately £27,432 in Income Tax and £5,006 in National Insurance contributions — a combined tax burden of around £32,438, or roughly 32.4% of your gross salary. Your effective (average) tax rate is approximately 32.4%, while the marginal rate on income just below £100,000 is 42% (40% IT + 2% NI).

Why is £100k considered a tax trap?

At £100,000, HMRC begins withdrawing the £12,570 Personal Allowance at a rate of £1 for every £2 earned above this threshold. This removal of tax-free income — combined with the 40% Higher Rate tax — creates an effective marginal rate of approximately 60% on income between £100,001 and £125,140. Earning a salary of exactly £100,000 is therefore often preferable to earning £105,000, unless the extra income is structured through pension contributions or other tax-efficient means.

How much National Insurance do you pay on £100k?

On a £100,000 salary, you pay approximately £5,006 in Class 1 National Insurance. This breaks down as: 8% on earnings between £12,570 and £50,270 (approximately £3,014), and 2% on earnings between £50,270 and £100,000 (approximately £992).

Is £100k a high salary in the UK?

Yes, by any objective measure. A £100,000 salary places you in the top 3–4% of UK earners. The UK median full-time salary is approximately £35,000, meaning a £100k earner takes home almost twice the median after tax. However, the experience of "being comfortable" on £100,000 is heavily influenced by location, family size, housing costs, and personal financial goals.

Do I need to file a Self Assessment tax return on £100k?

Yes. If your income exceeds £100,000, HMRC requires you to file a Self Assessment tax return each year, even if you are taxed through PAYE. This is also the mechanism through which you can claim Higher Rate relief on pension contributions, Gift Aid donations, and reclaim any overpaid tax.

Conclusion

A £100,000 salary is genuinely impressive — but as this guide has shown, the gap between gross and net pay is substantial. After Income Tax (approximately £27,432) and National Insurance (approximately £5,006), your take-home pay settles at around £67,562 per year, or £5,630 per month, under standard conditions.

The standout issue for earners at exactly this income level is the Personal Allowance trap. The withdrawal of the £12,570 allowance creates a 60% effective marginal rate on income between £100,001 and £125,140 — making smart tax planning essential, not optional.

The most impactful thing most £100k earners can do is make sufficient pension contributions to keep their taxable income at or below £100,000. This preserves the full Personal Allowance, delivers 40% tax relief on contributions, and builds retirement wealth simultaneously.

Bottom line: With the right financial planning — particularly around pension contributions, salary sacrifice, and ISA usage — a £100,000 earner can meaningfully increase their effective take-home and long-term wealth, while staying fully compliant with HMRC requirements.

£45K After Tax UK: What You Actually Take Home in 2026

£70000 After Tax UK Calculator (2026)

£55000 After Tax UK (2026) | Take-Home Pay Calculator