Inheritance tax often becomes a real concern for families only after the death of the second parent. While many estates pass tax-free when the first parent dies, the situation changes significantly once both parents have passed away. Understanding how inheritance tax works at this stage can help families avoid unexpected bills and ensure more of their estate passes to loved ones rather than HMRC.

This guide explains the UK rules in plain English, covering allowances, thresholds, and practical steps families should be aware of.

What Is Inheritance Tax in the UK?

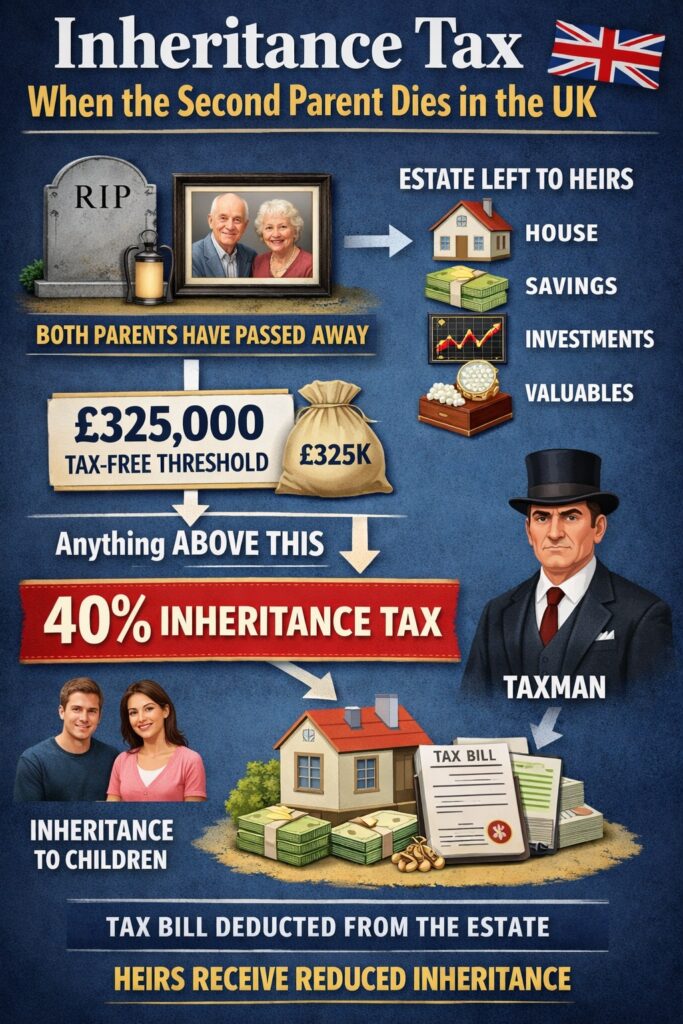

Inheritance tax, commonly known as IHT, is a tax charged on an estate after someone dies. An estate includes property, savings, investments, and personal belongings. In the UK, inheritance tax is usually charged at 40 percent on the value of the estate above a certain threshold.

This threshold is known as the Nil-Rate Band. As long as the total value of the estate stays below this amount, no inheritance tax is due. If it exceeds the threshold, tax is charged only on the portion above it, not on the entire estate.

For many families, inheritance tax does not apply at all, but rising property prices mean more estates are now crossing the tax threshold, particularly after the second parent dies.

Why Inheritance Tax Often Applies When the Second Parent Dies

When the first parent dies, assets are usually passed to the surviving spouse or civil partner. In most cases, this transfer is completely free from inheritance tax because of the spousal exemption. This means no inheritance tax is paid at that stage, regardless of the estate’s value.

However, this does not mean the estate escapes inheritance tax altogether. Instead, the tax is effectively postponed. When the second parent later dies, the combined value of all assets is assessed, including property, savings, and investments accumulated over both lifetimes. This is the point at which inheritance tax is most likely to apply.

Understanding the Nil-Rate Band

The Nil-Rate Band is the basic inheritance tax allowance available to everyone. It represents the amount of an estate that can be passed on tax-free. Any value above this allowance may be subject to inheritance tax.

One important feature of the Nil-Rate Band is that it can be transferred between spouses or civil partners. If the first parent did not use all or any of their Nil-Rate Band, the unused portion can be added to the allowance of the second parent’s estate.

This transfer does not happen automatically. The executors of the estate must claim it from HMRC when dealing with the second parent’s inheritance tax return. When claimed correctly, this can effectively double the tax-free allowance available.

The Residence Nil-Rate Band and the Family Home

In addition to the standard Nil-Rate Band, there is an extra allowance known as the Residence Nil-Rate Band. This applies when a main residence is passed on to direct descendants, such as children or grandchildren.

The purpose of this allowance is to reduce inheritance tax for families who want to pass on their home. Like the standard Nil-Rate Band, the Residence Nil-Rate Band can also be transferred between spouses if it was not used on the first death.

However, there are important conditions. The property must have been the deceased’s main residence at some point, and it must be left to direct descendants. There is also a limit for larger estates, as the allowance is gradually reduced once the estate exceeds a certain value.

£50000 After Tax UK: How Much Salary Do You Need?

How Much Can Be Passed on Tax-Free When the Second Parent Dies?

When all allowances are used correctly, a married couple or civil partners can pass on a significant amount of their estate without paying inheritance tax.

By combining both parents’ Nil-Rate Bands and Residence Nil-Rate Bands, families may be able to pass on up to £1 million tax-free. This usually includes the family home and other assets such as savings and investments.

If the estate exceeds this combined allowance, inheritance tax is normally charged at 40 percent on the excess. This is why proper planning and understanding of the rules is so important.

Real-Life Example – Meet the Williams Family

Let’s look at a real-life style example to make the rules easier to understand.

Emma and David Williams were a married couple living in London. When David passed away, he left his entire estate to Emma. Because of the UK’s spousal exemption, Emma did not have to pay any inheritance tax at that time, even though David’s estate included their home and savings. His inheritance tax allowances were also unused.

Emma lived for another 12 years after David’s death. During that time, London property prices increased significantly, and her savings continued to grow. By the time Emma passed away, her total estate was worth £1.05 million. This included a family home valued at £750,000 and savings of £300,000.

When handling Emma’s estate, her executors correctly claimed David’s unused Nil-Rate Band and Residence Nil-Rate Band. This gave the estate a combined inheritance tax allowance of £1 million. As a result, only £50,000 of the estate was subject to inheritance tax, rather than a much larger portion.

This careful application of the rules saved Emma’s children tens of thousands of pounds in inheritance tax. Without claiming the unused allowances, they could have faced an unnecessary tax bill of over £200,000, even though most of the estate was tied up in the family home.

The Williams family’s situation clearly shows why inheritance tax often becomes relevant only after the second parent dies and why understanding the UK inheritance tax rules early can make a major difference for the next generation.

How Much Does an Accountant Cost in the UK in 2026?

The Importance of Wills in Inheritance Tax Planning

Having a valid and up-to-date will is essential when it comes to inheritance tax. A well-written will ensures assets are distributed in a way that makes full use of available allowances.

Without a will, the estate is distributed according to intestacy rules, which may not align with inheritance tax efficiency. In some cases, this can result in higher tax bills or assets passing to unintended beneficiaries.

Wills also play a key role in ensuring the family home qualifies for the Residence Nil-Rate Band, particularly when there are complex family arrangements.

Other Ways Families Can Reduce Inheritance Tax

Inheritance tax planning does not start at death. Many families take steps during their lifetime to reduce the eventual tax bill. Gifting assets, using exemptions, and considering trusts are common strategies.

Regular gifting from surplus income and making use of annual gift allowances can gradually reduce the value of an estate. However, these strategies must be approached carefully, as some gifts can still be counted for inheritance tax if the person dies within a certain period.

Professional advice is often essential to ensure these steps are taken correctly and do not create unintended consequences.

Practical Steps to Take After the Second Parent’s Death

After the second parent dies, it is important to gather full details of the estate, including property values, savings, pensions, and investments. Executors should also locate records relating to the first parent’s estate, as these are needed to claim unused allowances.

Applying for transferred Nil-Rate Bands and Residence Nil-Rate Bands requires accurate paperwork and deadlines must be met. Mistakes or omissions can lead to higher tax bills than necessary.

Many families choose to work with probate specialists or tax advisers at this stage to ensure everything is handled correctly.

£35000 After Tax in the UK: What Your Salary Really Looks

Final Thoughts

Inheritance tax at the second parent’s death can come as a surprise, particularly for families who assumed everything was already taken care of when the first parent passed away. In reality, this is the point where inheritance tax planning matters most.

By understanding the available allowances, ensuring wills are in place, and taking professional advice when needed, families can significantly reduce or even eliminate inheritance tax. Planning ahead can make a meaningful difference, helping loved ones inherit more and face fewer financial worries during an already difficult time.